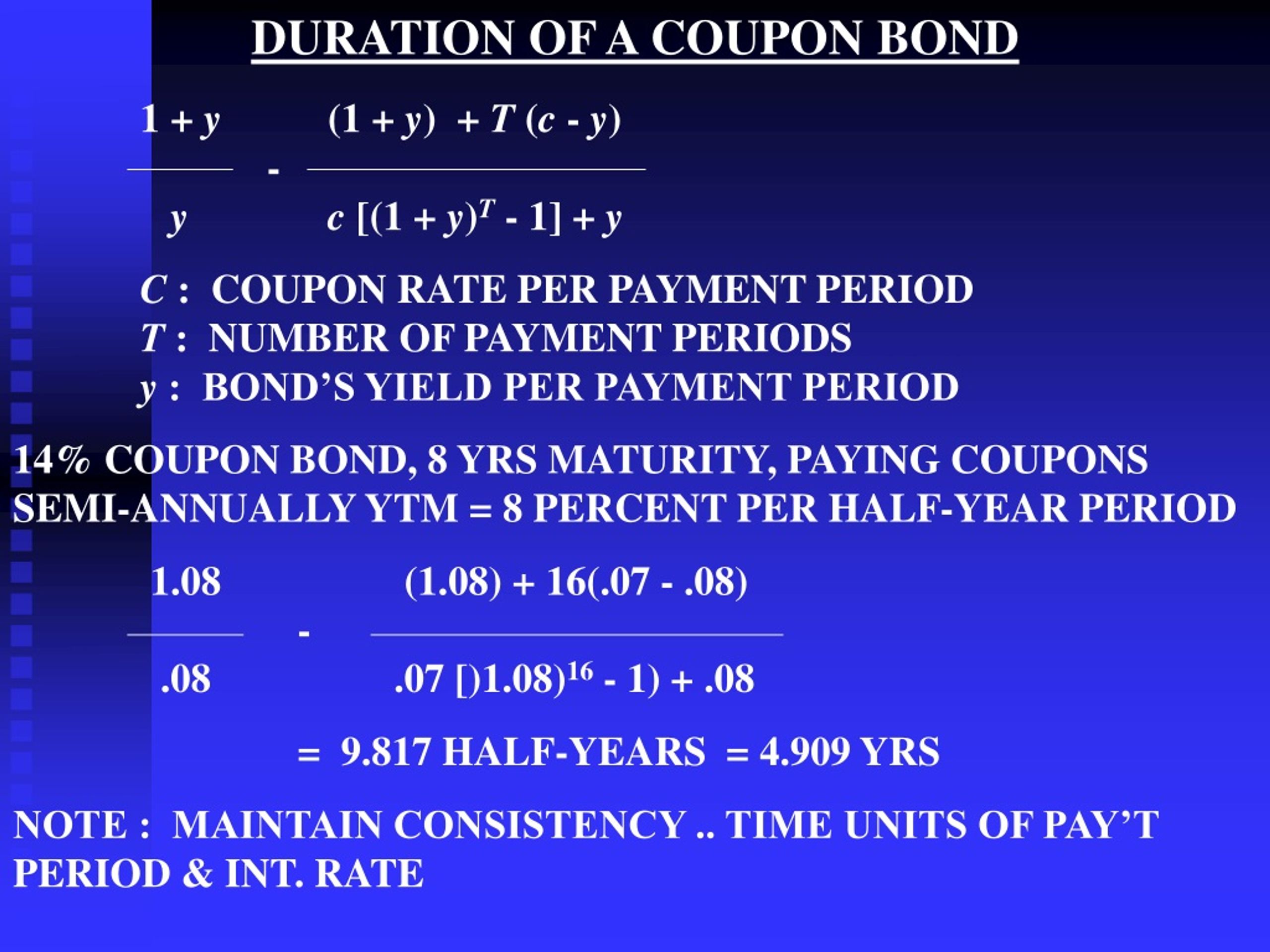

43 duration of a coupon bond

Bond Duration Calculator – Macaulay and Modified Duration From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity – it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ... 7 Best Tax-Free Municipal Bond Funds | Investing | U.S. News Aug 01, 2022 · A duration of 7.7 years for MANKX means that for every 1% increase or decrease in rates, the value of the fund will fall or rise by roughly 7.7%, respectively, as …

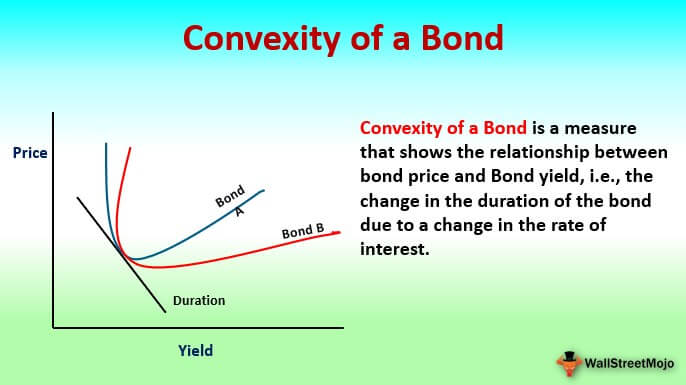

Convexity of a Bond | Formula | Duration | Calculation For a Bond of Face Value USD1,000 with a semi-annual coupon of 8.0% and a yield of 10% and 6 years to maturity and a present price of 911.37, the duration is 4.82 years, the modified duration is 4.59, and the calculation for Convexity would be:

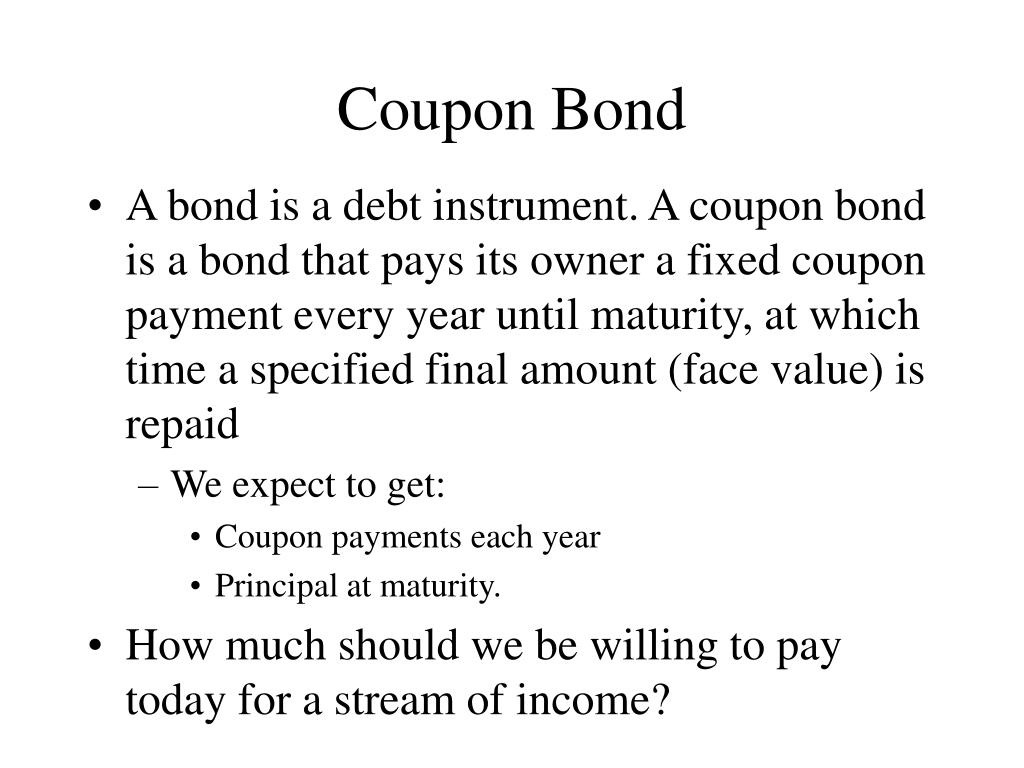

Duration of a coupon bond

Bond Convexity Calculator: Estimate a Bond's Yield Sensitivity Bond Price vs. Yield estimate for the current bond. Zero Coupon Bonds. In the duration calculator, I explained that a zero coupon bond's duration is equal to its years to maturity. However, it does have a modified (dollar) duration and convexity. Zero Coupon Bond Convexity Formula. The formula for convexity of a zero coupon bond is: Duration - Definition, Types (Macaulay, Modified, Effective) Jan 22, 2022 · It is a measure of the time required for an investor to be repaid the bond’s price by the bond’s total cash flows. The Macaulay duration is measured in units of time (e.g., years). The Macaulay duration for coupon-paying bonds is always lower than the bond’s time to maturity. For zero-coupon bonds, the duration equals the time to maturity. Duration Definition - Investopedia May 31, 2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ...

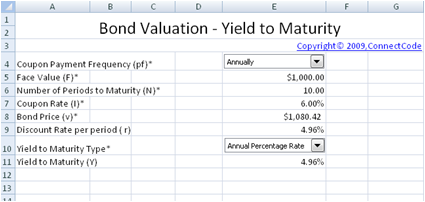

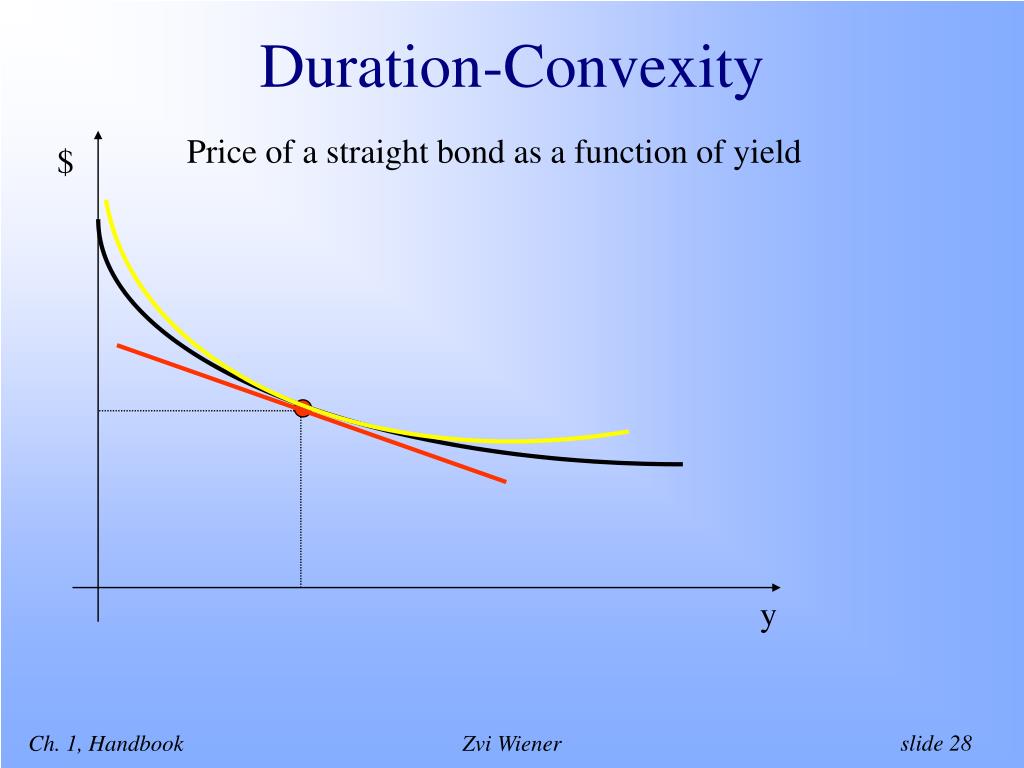

Duration of a coupon bond. Bond Valuation Definition - Investopedia May 31, 2022 · Bond valuation is a technique for determining the theoretical fair value of a particular bond. Bond valuation includes calculating the present value of the bond's future interest payments, also ... Understanding Bond Risk | FINRA.org Say you bought a 10-year, $1,000 bond today at a coupon rate of 4 percent, and interest rates rise to 6 percent. If you need to sell your 4 percent bond prior to maturity you must compete with newer bonds carrying higher coupon rates. These higher coupon rate bonds decrease the appetite for older bonds that pay lower interest. Coupon Definition - Investopedia Apr 02, 2020 · Coupon: The annual interest rate paid on a bond, expressed as a percentage of the face value. Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

Bond Price Calculator – Present Value of Future Cashflows - DQYDJ Using the Bond Price Calculator Inputs to the Bond Value Tool. Bond Face Value/Par Value - Par or face value is the amount a bondholder will get back when a bond matures.; Annual Coupon Rate - The annual coupon rate is the posted interest rate on the bond. In reverse, this is the amount the bond pays per year divided by the par value. Callable bond - Wikipedia A callable bond (also called redeemable bond) is a type of bond (debt security) that allows the issuer of the bond to retain the privilege of redeeming the bond at some point before the bond reaches its date of maturity. In other words, on the call date(s), the issuer has the right, but not the obligation, to buy back the bonds from the bond holders at a defined call price. How to Calculate the Bond Duration (example included) Jul 23, 2022 · FV = Bond face value; C = Coupon rate; t i = Time in years associated with each coupon payment; Once you calculated the Macaulay duration, you can then apply the following formula to get the Modified Duration (ModD): MacD ModD = (1+YTM/m) Example of calculating the bond duration. Imagine that you have a bond, where the: Bond Duration Calculator - Exploring Finance Bond face value is 1000 ; Annual coupon rate is 6% ; Payments are semiannually (1) What is the bond’s Macaulay Duration? (2) What is the bond’s Modified Duration? You can easily calculate the bond duration using the Bond Duration Calculator. Simply enter the following values in the calculator:

Duration Definition - Investopedia May 31, 2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ... Duration - Definition, Types (Macaulay, Modified, Effective) Jan 22, 2022 · It is a measure of the time required for an investor to be repaid the bond’s price by the bond’s total cash flows. The Macaulay duration is measured in units of time (e.g., years). The Macaulay duration for coupon-paying bonds is always lower than the bond’s time to maturity. For zero-coupon bonds, the duration equals the time to maturity. Bond Convexity Calculator: Estimate a Bond's Yield Sensitivity Bond Price vs. Yield estimate for the current bond. Zero Coupon Bonds. In the duration calculator, I explained that a zero coupon bond's duration is equal to its years to maturity. However, it does have a modified (dollar) duration and convexity. Zero Coupon Bond Convexity Formula. The formula for convexity of a zero coupon bond is:

Bond pricing - Bogleheads

Solved: A Bond With An Annual Coupon Rate Of 4.8% Sells Fo... | Chegg.com

PPT - Interest Rates and Returns: Some Definitions and Formulas ...

Professional Bond Valuation and Yield to Maturity spreadsheet

Solved: A Bond With An Annual Coupon Rate Of 5.3% Sells Fo... | Chegg.com

PPT - Chapter 13 BOND PORTFOLIO MANAGEMENT The Passive and Active ...

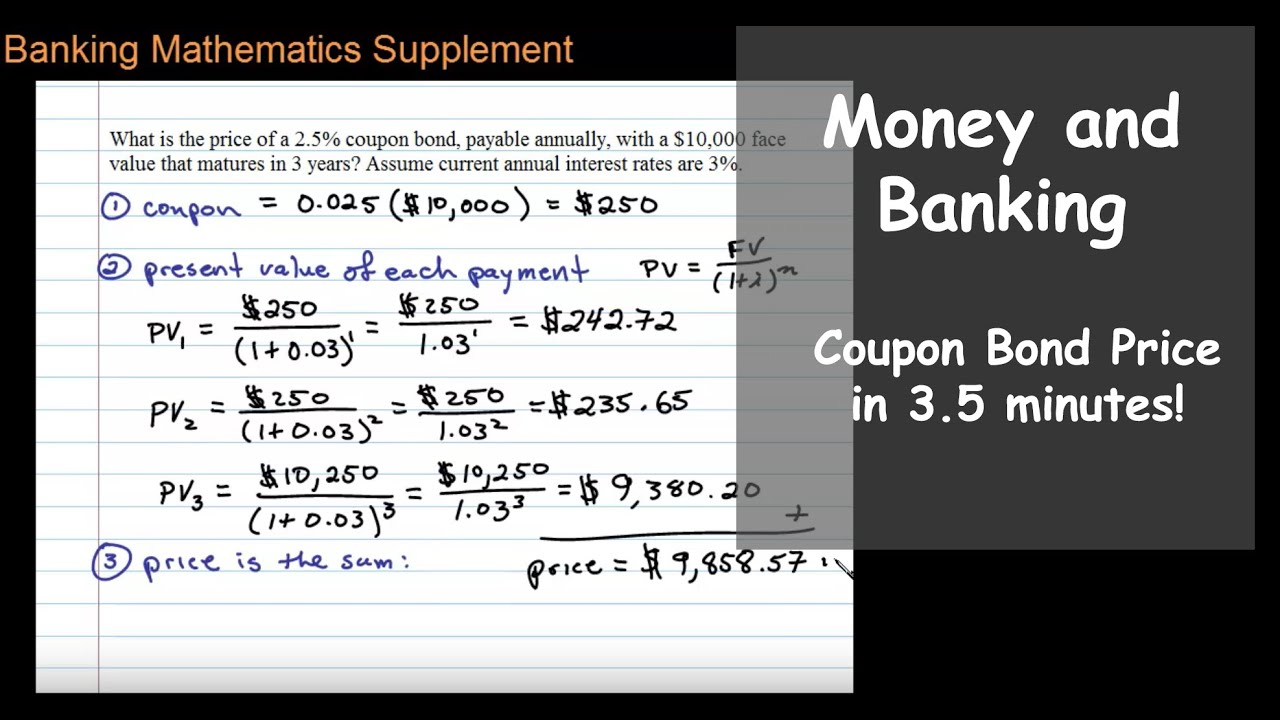

Coupon Bond Price - YouTube

Fixed Income: Spot Rate Calculation – Forward Rate Calculation ...

Convexity of a Bond | Formula | Duration | Calculation

0 Coupon Bond Formula ~ coupon

PPT - Financial Risk Management PowerPoint Presentation, free download ...

Managing Bond Portfolios: Bond Strategies, Duration, Modified Duration ...

Modified Duration (Definition, Formula)| Step by Step Calcuation Examples

Use Duration And Convexity To Measure Bond Risk

[Solved] Find the duration of a 8% coupon bond making annual coupon ...

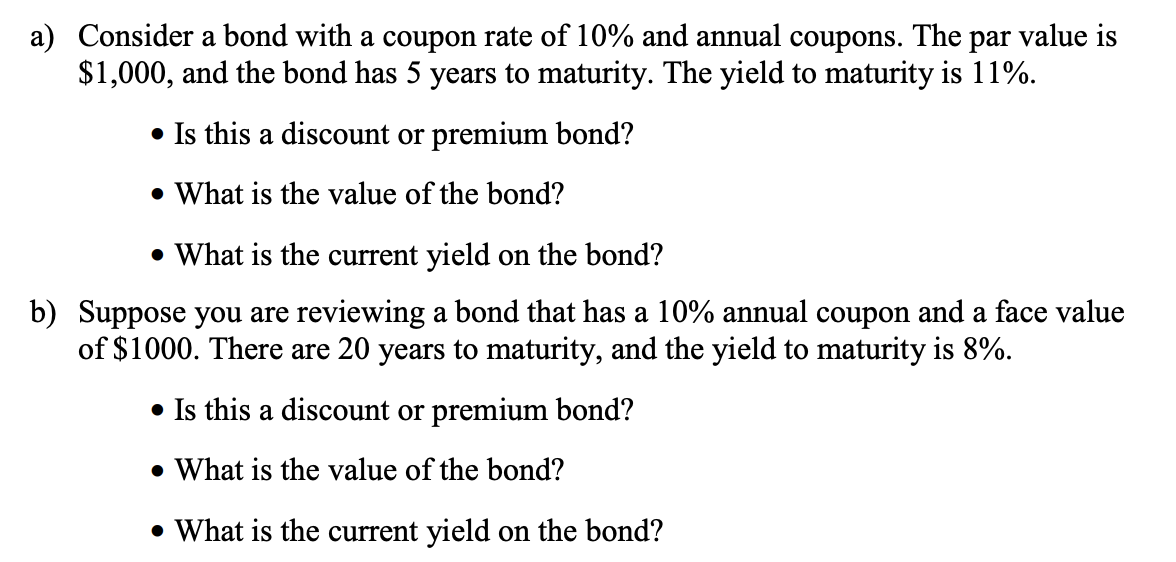

a) Consider a bond with a coupon rate of 10% and | Chegg.com

Post a Comment for "43 duration of a coupon bond"